Tax Benefits and Accelerated Depreciation

An Arizon air-supported building offers a number of financial benefits in addition to low cost-per-square-foot upfront pricing. There are important tax and depreciation benefits to consider when comparing an air-supported building to other types of construction. Such benefits may make an air-supported building more attractive, especially for new businesses.

If a structure is not inherently permanent, the property will be considered tangible personal property and not be subject to real estate taxes.

According to state and local taxing authorities, all property of its taxpayers is divided into two classes: real estate property and personal property.

Real estate property includes all land, building structures and other property that is a fixture to land or a building structure. Personal property, on the other hand, includes all things that are not real estate property. All real estate property is taxed by state, county and local governments, whereas personal property is not taxed at all or is taxed at a low rate.

One of the benefits of an Arizon air-supported building is that it can qualify as personal property by the Internal Revenue Service (IRS). See IRS service code section 1245. Personal property is not subject to real estate taxes.

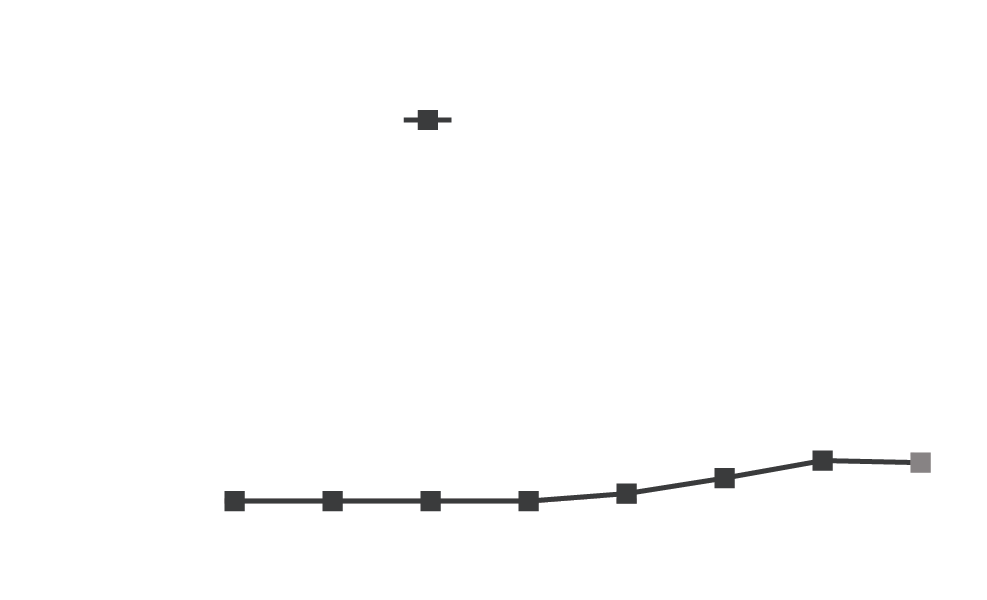

Depreciable Tax Savings of Air Structures vs. Conventional Buildings

Figures are based on an assumed cost of $1 million per structure at a tax rate of 40%. The allowable depreciation of an air structure in its second year of life is $244,900, resulting in tax savings of $97,960. In contrast, a similarly valued building only depreciates $25,641 in its second year, for a tax savings of only $10,256.

Tax Savings